If you’re a veteran exploring personal loan options, gaining a comprehensive understanding of the landscape can be invaluable. Let’s examine the various routes available and the key factors to consider.

Types of Personal Loans for Veterans

VA Personal Loans

Let’s start by examining VA personal loans, which are considered one of the most appealing choices for veterans. These loans, supported by the U.S. Department of Veterans Affairs, offer an interest rate as low as 2.87%, making them a highly enticing option.

With a proven track record of assisting more than 29 million veterans and service members in achieving homeownership, VA loans truly stand out. One of the reasons why VA loans are so appealing is that their eligibility criteria allow more veterans to qualify.

Moreover, they offer the advantage of no down payment and limited closing costs, contributing to their popularity among veterans. However, it’s important to consider that these loans come with funding fees and occupancy requirements that should be taken into account when making your decision.

Military Financial Institutions

Another avenue worth exploring is military-specific financial institutions, such as the Navy Federal Credit Union, which approved over 52,000 loans to veterans and active-duty members in 2020. These institutions focus exclusively on serving the military community and have a deep understanding of veterans’ unique circumstances.

The benefits of opting for military financial institutions include the potential for specialized loan products, reduced fees, and personalized guidance tailored to your needs. However, keep in mind that membership eligibility criteria may be more restrictive compared to other options.

Traditional Lenders

In addition to VA and military-specific options, veterans also have the choice to consider traditional lenders. Surprisingly, veterans often find it easier to secure loans from conventional banks and credit unions due to their steady income and benefits.

Traditional lenders like banks and credit unions may not offer specialized products for veterans, as the VA does. However, they provide convenience and widespread availability. This accessibility and flexibility can be crucial for borrowers who prioritize convenience in their loan application process.

When evaluating different personal loan options available to veterans, keep personal loan requirements a priority. Lenders assess factors like credit history, income, debts, and borrowing track record to determine if applicants meet requirements.

Qualifying for Personal Loans

Meeting eligibility criteria is pivotal for securing loan approval. We’ll provide an in-depth exploration of qualification factors.

Healthy Credit Scores Open Doors

The first factor lenders scrutinize is your credit score. You’ll typically need at least a 620 FICO score for approval. The good news for veterans is that their average score is 709, which is higher than the national norm of 695.

Stay on top of your credit by:

- Paying all bills by the due date

- Keeping credit card balances under 30% of limits

- Checking for errors in your credit reports

Proving Your Financial Fitness

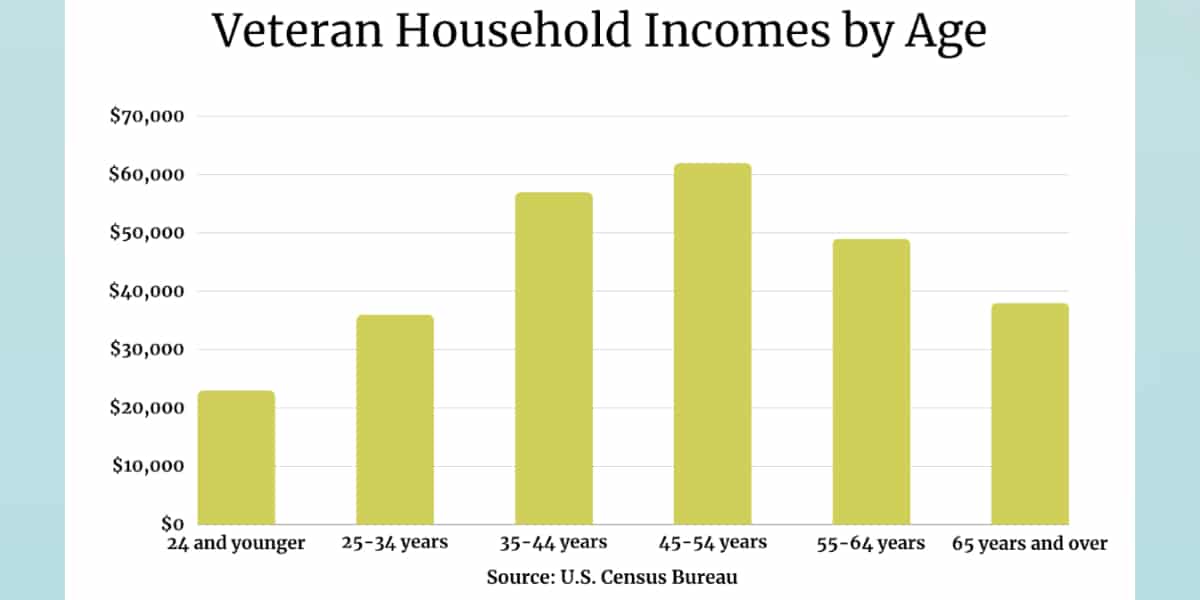

Lenders also confirm your income sources and job history. Submit documents like tax returns, recent pay stubs, and bank account statements. If you’re self-employed, provide two years of detailed business financial statements.

Median household incomes across veteran age groups also provide useful benchmarking data when documenting finances:

While personal loans don’t have set income requirements, you must demonstrate reliable income to manage the monthly payments. Talk to a loan officer about the specific documentation needed.

Overcoming Credit Challenges

If you’re working through credit issues, some options still exist. Federal credit counseling provides guidance to start strengthening your credit. Meanwhile, secured loan products allow borrowing against a vehicle or savings account as collateral.

Addressing credit obstacles now lays the foundation for qualifying for top-tier personal loan rates down the road. With persistence and healthy money management, loan approval could be within reach.

Understanding Interest Rates and Terms

Interest Rates

Let us shift gears and talk about interest rates. At the end of December 2021, the average 30-year fixed mortgage rate for VA loans stood at just 2.93%. What factors affect these rates, and how can veterans get the best deal?

Rates offered depend on certain factors, such as credit scores, income, loan amount, and terms. Comparing the options available from several lenders may show the lowest one. Veterans might prefer fixed interest rates over variable ones to keep their payments steady.

Loan Terms and Conditions

One of the key elements in making decisions is knowing the terms behind loans. For example, veterans should be aware that predatory lending practices can be a concern (Consumer Financial Protection Bureau). We will look into all aspects of loan agreements and potential pitfalls.

Checking the fine print for unusual fees, reviewing early repayment policies, and confirming lending licenses helps avoid unfavorable situations. When necessary, financial advisors can offer their expertise.

Applying for Personal Loans

Once you understand the qualification benchmarks, the next crucial step is navigating the loan application process. Compiling documents, selecting lenders, completing applications properly, and planning for timelines will pave the way forward.

Preparing Documentation

To avoid application delays, having key paperwork ready provides efficiency. Critical documents include:

- DD-214 discharge papers

- Tax returns from the last 2 years

- Recent pay stubs and bank statements

- Retirement benefit letters

- Profit and loss statements (for self-employed)

Also, obtaining a Certificate of Eligibility from VA.gov will facilitate applying for VA loans specifically.

Choosing Lenders

The next task entails selecting lenders to apply with. Casting a wide net and submitting applications to multiple lenders will expand options and chances for approval. Excellent starting points include VA.gov for specialized offerings, Pentagon Federal Credit Union or Navy Federal for military-focused products, and national banks like Bank of America, Wells Fargo, or U.S. Bank for conventional lending alternatives.

Submitting Error-Free Applications

With target lenders selected, submitting comprehensive, accurate applications follows. Double-checking entries for errors will help avoid processing delays or complications. Having bank statements, tax returns, and identification documents ready for submission will also facilitate smooth sailing.

Managing Timelines

Lastly, anticipating processing timelines will simplify planning. While timeframes vary, approval for secured loans or smaller sums may only take 1-2 weeks. Larger unsecured loans could take 60-90 days, however – especially via the Small Business Administration (SBA). It’s crucial to apply well in advance of your financial needs.

Tracking applications through online portals and maintaining ongoing communication with loan officers will keep the process on track, especially when navigating potential snags. With diligence, veterans can carefully orchestrate financing crucial for advancing important pursuits.

Conclusion

In conclusion, veterans exploring personal lending have a range of options, from VA offerings to conventional products. While VA loans remain highly advantageous, military-focused institutions and traditional lenders alike can provide key benefits.

Checking eligibility, securing favorable interest rates and terms, and completing applications set the stage for loan approval. Even when facing obstacles, alternative pathways can help veterans pursue accessible financing. Through informed decision-making, veterans can responsibly utilize personal loans to support their life endeavors.

Frequently Asked Questions (FAQs)

- What is the minimum credit score required to qualify for a VA personal loan?

Typically, a minimum credit score of 620 is needed for VA loan approval. However, requirements can vary by lender.

- Can veterans with a history of bad credit still secure a personal loan?

Yes, those with poor credit may still qualify for specialized Veterans Affairs loans or high-risk offerings from certain lenders. Improving credit scores will expand eligible loan options.

- How do interest rates and eligibility for VA personal loans compare to traditional lender loans?

VA loans could potentially offer lower interest rates and have more flexible eligibility criteria tailored specifically to veterans and service members.

Published by: Martin De Juan